Chapter 11 Code#

We begin with some imports

import numpy as np

import matplotlib.pyplot as plt

from numba import njit

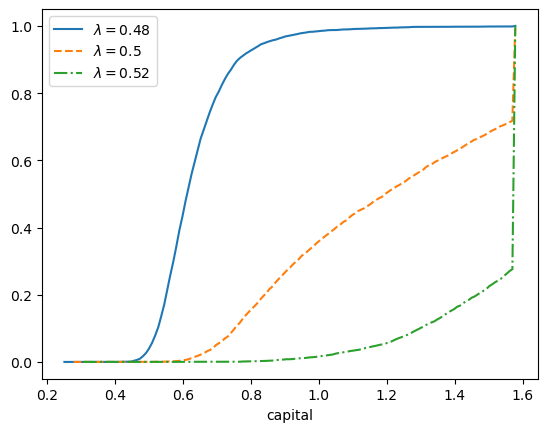

Now we recreate figure 11.3. Our first step is to set the parameters.

alpha = 0.6

Q = 2

R = 1

sigma = 0.1 # variance

mu = - sigma**2 / 2

Next we introduce useful functions.

@njit

def wage(k, z):

return (1 - alpha) * (k**alpha) * z

@njit

def theta(w, lda):

if (w < 1 - lda):

return lda / (1 - w)

else:

return 1

@njit

def g(y):

return (y/alpha)**(1/(alpha-1))

@njit

def update(k, z, lda):

" Update the state."

return g(R / (Q * theta(wage(k, z), lda)))

@njit

def a(lda):

return g(R / (lda * Q))

@njit

def generate_ts(lda, init=None, seed=1234, ts_length=10_000):

" Generate a time series from the model."

np.random.seed(seed)

K = np.empty(ts_length)

if init is None:

init = a(lda)

K[0] = init

for t in range(ts_length-1):

z = np.exp(mu + sigma * np.random.randn())

K[t+1] = update(K[t], z, lda)

return K

Now we recreate the plot.

b = g(R / Q)

lambdas = 0.48, 0.5, 0.52

line_type = '-', '--', '-.'

mc_size = 5000

grid_size = 150

fig, ax = plt.subplots()

for lda, lt in zip(lambdas, line_type):

xvec = np.linspace(a(lda), b, grid_size)

obs = generate_ts(lda, ts_length=mc_size)

def ecdf(y):

return sum(obs <= y) / mc_size

yvec = [ecdf(x) for x in xvec]

ax.plot(xvec, yvec, lt, label=rf'$\lambda={lda}$')

ax.set_xlabel('capital')

ax.legend()

plt.show()

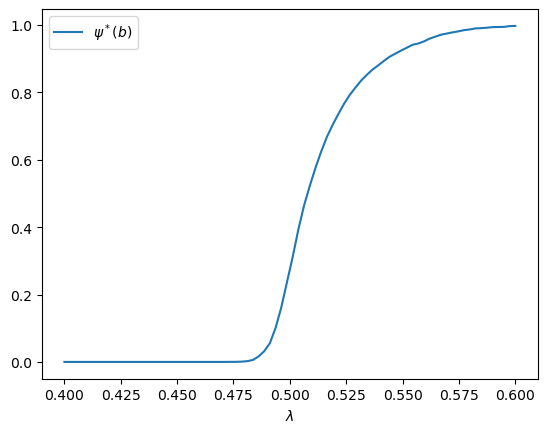

Now we address exercise 11.26.

We need to determine the fraction of time the sample spends at the point \(b\) in the state space over a long horizon, for different values of \(\lambda\).

grid_size = 80

lambdas = np.linspace(0.4, 0.6, grid_size)

mc_size = 5000

prob_at_b = np.empty_like(lambdas)

for i, lda in enumerate(lambdas):

obs = generate_ts(lda, ts_length=mc_size)

prob_at_b[i] = np.mean(obs == b)

fig, ax = plt.subplots()

ax.plot(lambdas, prob_at_b, label=r'$\psi^*({b})$')

ax.set_xlabel(r'$\lambda$')

ax.legend()

plt.show()